For a small business owner, the phrase “regulatory compliance” probably sounds like a headache waiting to happen. It brings to mind stacks of paperwork and rules that seem designed to slow you down. But I want to offer a different perspective: think of compliance as a fundamental shield that protects your business from fraud, fines, and a damaged reputation.

Getting a handle on Know Your Customer (KYC) and Know Your Business (KYB) isn’t just about appeasing regulators. It’s about building a solid, trustworthy company from the ground up.

Why Compliance Is a Shield, Not a Burden

Let’s be honest, compliance can feel like a maze of legalese, especially when you’re already juggling a dozen other tasks. But at its core, it boils down to one simple, common-sense idea: know who you’re doing business with. It’s no different than checking someone’s ID before you hand them the keys to a rental car.

These verification processes, KYC and KYB, are your first line of defense. By simply collecting and confirming a few key documents, you can be reasonably sure that your customers and partners are who they say they are. This one step is incredibly powerful. It helps you weed out bad actors, steer clear of scams, and build a solid foundation of trust with the right people.

The Real Risks of Looking the Other Way

Brushing off KYC and KYB is more than a small slip-up; it leaves your business wide open to some pretty serious threats. Without a system in place, you could easily get tangled up with individuals or companies involved in financial crime, and the fallout can be disastrous.

- Hefty Fines: Regulators don’t mess around. The financial penalties for non-compliance can be crippling for a small business.

- Lost Trust: Once your reputation is tarnished by a compliance issue, it’s incredibly difficult to win back the trust of customers and partners.

- Major Distractions: Getting audited or investigated can bring your business to a screeching halt, consuming time and money you should be spending on growth.

Think of compliance like a smoke detector in your office. You hope you never have to hear it go off, but you’re glad it’s there. It’s a proactive investment that provides a critical early warning, saving you from a potential disaster down the road.

The rules are also constantly changing. For example, in just one month, there were at least 264 regulatory updates related to privacy alone across the globe. Keeping up is a real challenge, but it’s not optional.

Turning Compliance into a Competitive Edge

Instead of dreading document collection, what if you saw it as an opportunity? When you have a smooth, professional compliance process, you send a powerful message. It tells clients and partners that you’re a serious, secure, and well-run organization.

This is where having a good system makes all the difference. An efficient approach isn’t about ticking boxes—it’s about creating an onboarding experience that is both secure and painless. To make this happen, many small businesses are turning to smart tools. For example, setting up a vendor compliance document portal can centralize and simplify how you gather and manage all that crucial information.

When you shift your mindset and see compliance as your shield, you start building a stronger, more resilient business ready for whatever comes next.

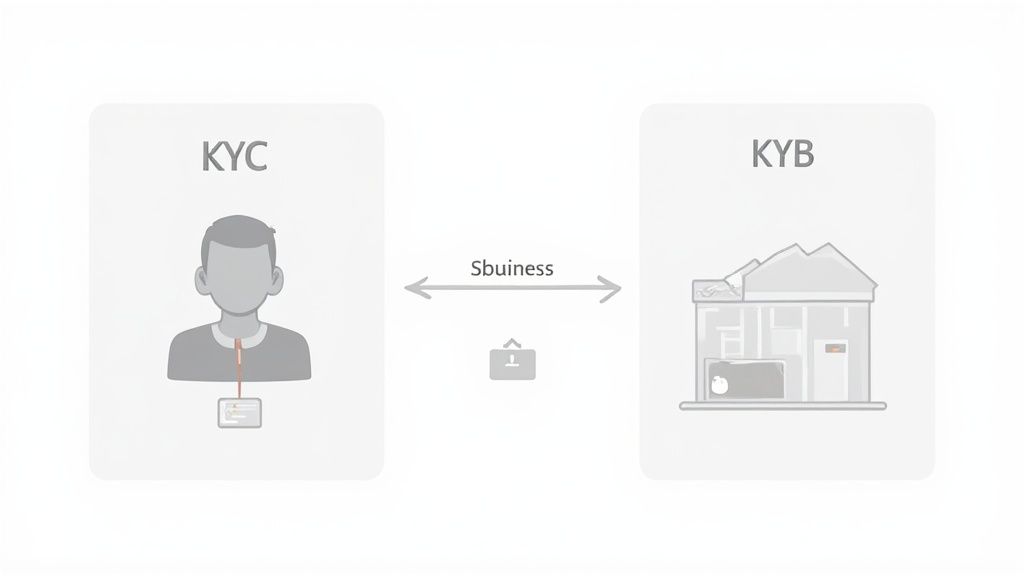

Getting to Know Your Customers: KYC and KYB Explained

When you first hear about compliance for small companies, you’ll quickly run into two acronyms: KYC and KYB. They might sound technical, but the idea behind them is simple. They’re two sides of the same coin, both centered on one fundamental principle: you need to know who you’re doing business with.

Think of it this way: KYC is for people, and KYB is for businesses.

Getting this distinction right is your first real step toward building a compliance process that actually works. Know Your Customer (KYC) is all about making sure your individual clients are who they say they are. It’s the same reason a bank asks for your driver’s license when you open an account.

Know Your Business (KYB) takes that same logic and applies it to your corporate clients. You’re verifying that the company is a real, registered entity and, just as importantly, figuring out who is pulling the strings behind the scenes. This is how you avoid accidentally partnering with a shell company designed for shady activities.

The Core Documents for KYC

When you’re onboarding an individual, the paperwork is usually pretty straightforward. Your job is to collect official documents that prove their identity and where they live. These two pieces of information are the bedrock of your due diligence.

Here are the must-haves for a standard KYC check:

- Proof of Identity: You’ll need a valid, government-issued photo ID. A passport, driver’s license, or national ID card is the gold standard here.

- Proof of Address: This document connects the person to a physical location. A recent utility bill, bank statement, or rental agreement usually does the trick, as long as it’s dated within the last three months.

By collecting and checking these documents, you create a baseline of trust and tick a major regulatory box. It’s a simple process that goes a long way in preventing fraud.

KYC isn’t about putting up walls for good customers. It’s about starting the relationship with a verifiable, transparent handshake. That proof protects both you and your client from risk down the line.

Remember, when you collect this personal data, you’re also responsible for protecting it. Ensuring you have a secure process for handling sensitive information is an invaluable step to make sure you’re handling everything correctly.

The Essential Paperwork for KYB

Verifying a business is a little more complex because you have to look past the company name and understand its structure and ownership. Your goal is to confirm its legal standing and identify the people who actually own and control it.

Your KYB document checklist should include:

- Proof of Business Registration: This is the official paperwork proving the company legally exists. It could be their Articles of Incorporation, a Certificate of Good Standing, or a state-issued business license.

- Proof of Business Address: Just like with an individual, you need to verify the company’s physical operations. A recent utility bill, lease agreement, or bank statement with the company’s name on it works perfectly.

- Ownership Information: This is the critical step. You need to identify the Ultimate Beneficial Owners (UBOs)—that is, any person who ultimately owns or controls more than 25% of the company. Often, this means you’ll need to collect their personal IDs, circling you right back to a KYC check on them.

This process is your best defense against getting mixed up with businesses involved in money laundering or other financial crimes.

KYC vs. KYB At a Glance

While KYC and KYB both focus on verification, they differ in scope and complexity. Knowing these differences helps you build a smarter, more efficient onboarding process for every type of client.

Here’s a simple breakdown to see how they compare.

| Aspect | KYC (Know Your Customer) | KYB (Know Your Business) |

|---|---|---|

| Target | Individual clients and customers. | Business clients, partners, and vendors. |

| Primary Goal | To verify a person’s identity and assess their individual risk profile. | To verify a company’s legal status, operational legitimacy, and ownership structure. |

| Key Documents | Government-issued photo ID and a recent proof of address. | Business registration documents, proof of address, and identification for beneficial owners. |

| Main Risk Averted | Identity theft, personal fraud, and transactions with sanctioned individuals. | Money laundering, shell companies, and association with illicit corporate entities. |

At the end of the day, getting both KYC and KYB right is non-negotiable for running a responsible business. It sends a clear signal to regulators, partners, and legitimate customers that you’re serious about security and integrity—a cornerstone of any successful company.

Building Your Document Collection Workflow

Knowing the rules of KYC and KYB is one thing, but actually putting them into practice is where it all comes together for a small business. A solid document collection workflow is the heart of your compliance program—it’s your step-by-step process for requesting, gathering, and checking essential information from every new client.

Think of it as your assembly line for building trust. Each step is designed to be efficient, secure, and most importantly, repeatable. Without a set process, you’re constantly reinventing the wheel, which opens the door to mistakes, delays, and serious security gaps. A formal workflow brings calm to the chaos.

And don’t worry, this doesn’t have to be complicated. It’s about setting up a smart system from the start that protects your business, gives clients peace of mind, and makes your life easier.

Identifying the Right Documents for Your Business

First things first: you need to know exactly what to ask for. The specific KYC and KYB documents you’ll need will change based on your industry, the kind of services you provide, and how much risk you think a client represents. Someone low-risk might only need to show basic ID, while a more complex client will require a much deeper look.

The best way to handle this is by creating a simple, tiered checklist. This keeps your team on the same page and ensures you collect the right information every time.

- Tier 1 Basic Verification (Low-Risk Individuals): For most individual customers, you just need the basics. This usually means a government-issued photo ID (like a passport or driver’s license) and something to prove their address, like a recent utility bill.

- Tier 2 Basic Verification (Low-Risk Businesses): When you onboard a small business, you’ll want to see its official registration papers, proof of its operating address, and its tax ID number. This confirms it’s a legitimate entity.

- Tier 3 Enhanced Verification (Higher-Risk Clients): For businesses in sensitive industries or those with complicated ownership structures, you have to dig a bit deeper. That means identifying the Ultimate Beneficial Owners (UBOs)—the people who actually own or control the company—and collecting their personal KYC documents, too.

A documented collection policy is your best defense in an audit. It demonstrates that you have a thoughtful, risk-based approach to client verification, rather than just an arbitrary or inconsistent process.

Securely Requesting and Receiving Information

How you ask for and receive sensitive documents is just as important as what you’re asking for. Collecting copies of passports and bank statements over standard email is a massive security risk. Email isn’t encrypted, which means your clients’ data is exposed and your inbox becomes a goldmine for hackers.

Ditching email for document collection isn’t just a “nice-to-have”—it’s a critical step in protecting your business and earning your clients’ trust. Using safer, more professional tools creates a secure and organized system for everyone involved.

Here are a couple of much safer alternatives:

- Secure Client Portals: A dedicated portal gives your clients a single, encrypted place to upload their documents. It keeps all that sensitive information out of vulnerable email chains.

- Specialized Document Collection Software: Platforms built specifically for this purpose offer the best security and efficiency. They often come with handy features like automatic reminders and validation checks.

For small businesses ready to level up their process, looking into KYC document collection software can provide a powerful and secure solution right out of the box.

Verifying Documents and Spotting Red Flags

Once you have the documents in hand, the next job is to verify them. This doesn’t mean you need expensive forensic tools. For most small companies, verification starts with simple, manual checks to catch obvious fakes or errors.

Your verification checklist should include a few non-negotiable checks:

- Check Expiration Dates: Are the IDs or licenses still valid? This is a quick and easy first look.

- Match Names and Addresses: Does the name and address on the utility bill match what’s on their ID and what they told you?

- Look for Tampering: Give the documents a good visual inspection. Look for anything that seems off, like mismatched fonts, blurry spots, or sloppy photo edits.

- Confirm Business Registration: For business clients, you can often use public databases (like the Secretary of State’s website in the US) to confirm the business is officially registered and in good standing.

Taking these steps wraps up your workflow. By creating a clear, secure, and repeatable process to identify, request, and verify documents, you build a compliance foundation that protects your business from risk and makes onboarding a breeze.

Staying Organized and Ready for an Audit

Getting your compliance in order isn’t a “set it and forget it” task. It’s an ongoing practice. Once you have a smooth process for collecting documents, the real work begins: keeping everything organized and ready for inspection at a moment’s notice. An audit shouldn’t be a mad dash to find paperwork; it should just be a routine check-up that confirms all the great work you’re already doing.

This is all about shifting your thinking. You’re not just a document collector; you’re a document manager. A well-oiled system is the best way to show you take compliance for small companies seriously, turning a potential headache into just another part of doing business.

A Quick and Simple Risk Assessment

Let’s be honest, not all clients are the same, and your compliance efforts shouldn’t treat them that way either. A simple risk assessment is your way of figuring out which clients need a little more attention—a process often called enhanced due diligence (EDD). This isn’t about being paranoid; it’s about using your time and energy wisely.

Think of it like a home security system. For most visitors, the standard setting is fine. But for some, you might need to activate a few extra sensors.

Here’s a straightforward way to group your clients by risk:

- Low-Risk Clients: These are your bread-and-butter customers. Think local businesses or individuals with easy-to-verify information. Your standard KYC/KYB checks are perfectly fine here.

- Medium-Risk Clients: This group might include businesses in cash-heavy industries or those with slightly more complicated ownership structures. For them, you might want to double-check their information a bit more often.

- High-Risk Clients: These clients require your full attention from day one. They might operate in industries known for financial trouble, be based in high-risk countries, or have a corporate structure that’s hard to untangle.

Secure Record-Keeping and Retention

After you’ve collected and verified a document, your job isn’t done. You need a secure, organized place to keep all this sensitive information. This is a common trip-up for many small businesses.

Your record-keeping policy really just needs to answer three simple questions:

- What do I keep? Hold onto all your KYC and KYB documents, plus notes on your verification process and any risk assessments you’ve done.

- How long do I keep it? A good rule of thumb is to keep records for at least five years after you stop doing business with a client. But rules can change depending on where you are, so always check your local regulations.

- How do I store it safely? Storing documents online is the easiest way to go, but security is non-negotiable. Use systems with encryption and controlled access—never, ever leave sensitive files in an open shared drive or your email inbox.

A tidy record-keeping system does more than just get you ready for an audit. It gives you one central, trusted place for all client information, making your daily operations smoother and more secure.

Your Small Business Audit Readiness Checklist

The pressure on small companies to prove they’re compliant has ramped up significantly. While bigger companies might face four or more audits a year, small businesses usually handle two or three, and each one takes a toll. In fact, with the compliance data market expected to reach $16.6 billion, it’s clear that getting organized is more important than ever.

The best way to stay prepared is to use a checklist. A solid compliance audit checklist can be your guide to a painless review process.

Here are the absolute must-haves you should be able to pull up instantly:

- Written Policies and Procedures: Do you have your KYC, KYB, and risk assessment process written down? An auditor will almost certainly ask to see this first.

- Complete Client Files: Check that every client file has all the necessary ID documents, your verification notes, and a clear risk rating.

- Record of Ongoing Monitoring: Can you prove that you check in on client information from time to time, especially for your higher-risk clients?

- A Secure Storage System: Be prepared to show exactly how you protect sensitive data, including who can access it and how it’s encrypted.

- Employee Training Records: Keep a record showing that your team has been trained on your company’s compliance rules.

Keeping these items in order flips the script on audits. Instead of being a threat, an audit becomes your chance to show you’re a professional who does business the right way.

Using Automation to Simplify Compliance

For a small team, manually handling KYC and KYB compliance can feel like trying to fill a swimming pool with a teaspoon. It’s a huge drain on time and resources that you’d much rather spend on actually growing the business. This is where the right technology becomes your most valuable player, turning those repetitive, error-prone tasks into a smooth, automated workflow.

Imagine a system that automatically asks new clients for the right documents, sends out polite reminders so you don’t have to, and flags anything that’s missing for your attention. This isn’t about getting bogged down in complex, enterprise-level software. It’s about using smart, simple tools to save countless hours, slash human error, and create a professional, secure experience that builds client trust from day one.

The Old Way vs. The Smart Way

So many small businesses start out tracking compliance with a spreadsheet and chasing documents through endless email chains. It seems simple enough at first, but this manual approach quickly turns into a major bottleneck. Emails get buried, attachments go missing, and just keeping track of who sent what becomes a full-time job.

This method isn’t just inefficient; it’s a real risk. Sensitive client data is left sitting in unsecured inboxes, and the chances of a crucial detail slipping through the cracks are incredibly high.

Now, picture a streamlined, automated platform. Instead of chaos, you have a central, secure hub for every compliance-related task. It builds a perfect, audit-ready record of every interaction without you having to lift a finger. This single shift turns compliance for small companies from a messy chore into a polished, professional process.

How Automation Handles the Heavy Lifting

An automated document collection tool can take over the most tedious parts of your KYC and KYB process. Think of it as a digital assistant that ensures every step is completed consistently and securely, every single time.

Here are the key tasks automation can take off your plate:

- Automated Requests: Instead of writing individual emails, you set up templates that automatically request the specific documents needed from each client based on their risk profile.

- Polite Reminders: The system sends out scheduled follow-ups to clients who haven’t submitted their info yet, saving you from those awkward chase-up calls.

- Secure Submissions: Clients get a branded, secure link to upload their documents directly, which keeps their sensitive data out of vulnerable email inboxes.

- Centralized Dashboard: All submitted documents are neatly organized in one place, giving you a clear, at-a-glance view of your entire compliance pipeline.

- Expiration Tracking: The platform can monitor document expiration dates (like passports or business licenses) and automatically ask for updated versions before they expire.

Automation isn’t about replacing human oversight; it’s about freeing up your team to focus on what actually matters. When a system handles the repetitive work, you can spend your time on higher-value activities, like building client relationships and making informed risk assessments.

Closing the Compliance Gap for Small Businesses

Larger companies are adopting automation at a rapid pace, which is creating a real divide. While 56% of large enterprises are expected to move their compliance systems to the cloud, small businesses often lag behind because of limited resources. This gap is a big deal, as automated solutions are shown to cut compliance delays by 50% in bigger firms. For smaller companies sticking with manual methods, this exposes them to a much higher risk of noncompliance, penalties, and damage to their reputation. You can dig deeper into these trends with these critical compliance stats for 2025.

What to Look for in a Compliance Automation Tool

When you’re choosing a tool to help with compliance, you don’t need something with a thousand features you’ll never touch. For most small businesses, the best solutions are the ones that are simple, secure, and easy to get up and running.

Here’s a quick checklist of features that deliver the most value.

| Feature | Why It Matters for Small Businesses |

|---|---|

| Customizable Workflows | Lets you build a collection process that actually matches your specific KYC and KYB needs, rather than forcing you into a rigid, one-size-fits-all box. |

| Branded Client Portal | A professional, white-labeled portal for document submission reinforces your brand and builds client trust by showing you take their security seriously. |

| Secure, Encrypted Storage | Ensures all client data is protected both in transit and at rest, helping you meet data protection rules and avoid costly breaches. |

| Simple Integration | The ability to connect with other tools you already use (like your email or cloud storage) makes it much easier to fit into your daily operations. |

By embracing simple automation, you’re not just making your life easier. You’re building a more resilient, professional, and trustworthy business that can meet its regulatory obligations with confidence.

A Few Common Compliance Questions, Answered

Once you get the hang of KYC and KYB, the real questions start to pop up. It’s one thing to know the theory, but another to handle the day-to-day situations that come your way. Here are some straightforward answers to the questions we hear most often from small businesses.

Think of this as your practical cheat sheet. The goal is to clear up any gray areas so you can move forward with confidence, knowing you’re applying the rules correctly in the real world.

What Happens If We Fail a Compliance Audit?

Let’s be direct: failing a compliance audit is a big deal, and the consequences can sting. The most obvious hit is financial. Regulators can issue anything from a formal warning to a hefty fine that could seriously hurt a small business.

But the pain doesn’t stop there. Regulators might put restrictions on your operations, like blocking you from bringing on new clients until you prove you’ve fixed the problems. Honestly, the worst damage is often to your reputation. Word gets around, and a compliance failure can make potential customers and partners think twice before trusting you.

The best defense is a good offense. Regulators are much kinder to businesses that have a documented, good-faith effort to stay compliant—even if it’s not perfect—than to those with no real process at all.

How Often Should We Re-Verify Our Clients?

There’s no magic number here. The right answer depends entirely on how risky a client is. The smartest way to handle this is to create a schedule based on risk, which helps you focus your energy where it matters most.

A simple tiered system works wonders for most businesses:

- Low-Risk Clients: For your straightforward, everyday clients, checking in every two to three years is usually fine.

- Higher-Risk Clients: For clients in tricky industries or those with complicated ownership structures, an annual review should be your standard.

You should also have a plan to re-verify a client when something big changes. For a business client, that could be a new owner. For an individual, it might be a sudden, weird spike in their transaction activity. Just be sure to write this policy down so you can apply it consistently.

Is It Safe to Use Email for Document Collection?

In a word, no. Using regular email to ask for sensitive documents—passports, bank statements, you name it—is a huge security risk. Standard email isn’t encrypted, which means that information is basically flying through the internet unprotected, where it can be intercepted.

If there’s a data breach and that sensitive info gets out, your business could be held responsible for not protecting it properly. That can lead to major fines and, even worse, a total loss of client trust. To get a better handle on what’s required, understanding the key compliance requirements for businesses is a great place to start.

The right way to do this is with a secure, encrypted tool built for the job. A dedicated client portal or a document collection platform ensures that sensitive data is protected from start to finish. It’s professional, it’s secure, and it shows your clients you take their privacy seriously.

Ready to build a compliance workflow that’s simple, secure, and professional? Superdocu automates the entire document collection process, from branded requests to secure storage, freeing you to focus on your business. Discover how Superdocu can transform your compliance process today!