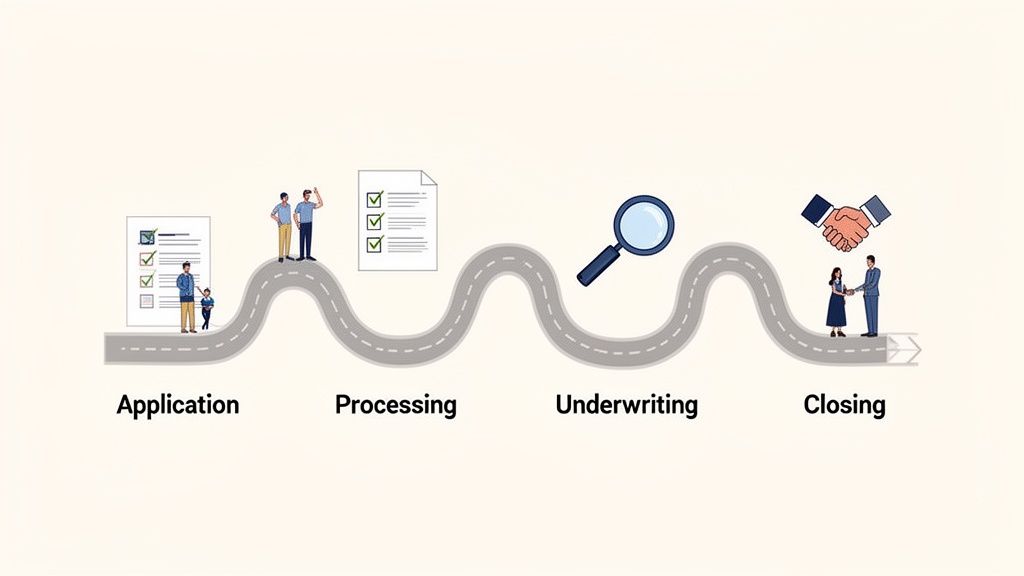

So, you want to understand the journey a mortgage application takes from start to finish? It's a structured path with four distinct stages: application, processing, underwriting, and finally, closing. Think of it as a relay race where the baton—the loan file—is passed from one expert to another, with each one verifying crucial details about the borrower's finances and the property itself.

Your Essential Roadmap to Mortgage Loan Processing

For anyone new to the industry, the mortgage process can feel like a maze of paperwork and unfamiliar terms. This guide will walk you through the entire workflow, breaking down what happens at each stage and clarifying the roles of the loan officer, processor, and underwriter. Getting a handle on this sequence is the secret to a smooth, on-time closing.

This is your starting point for mastering a process that turns a hopeful application into a homeowner's dream come true. Each step logically builds on the one before it, which is why a well-organized approach is so important for everyone involved.

At its core, getting a mortgage approved is all about verification. Lenders need to be certain of two things: that the borrower can actually afford to repay the loan, and that the property is worth what they’re lending against it. The entire process is designed to confirm those two points.

On average, you can expect a loan to take anywhere from 30 to 60 days to close. Of course, that timeline can shrink or stretch depending on how complex the file is and how efficiently the team works together.

To give you a bird's-eye view, let's break down the four main phases.

The Four Core Phases of Mortgage Processing

This table offers a quick snapshot of the entire journey. Understanding what happens in each phase—and why—is the first step to mastering the workflow.

| Phase | Primary Goal | Key Activities |

|---|---|---|

| Application | Gather the borrower's initial financial information and property details. | Completing the loan application, collecting income/asset documents, running credit reports. |

| Processing | Verify all information and prepare a complete, organized file for underwriting. | Ordering appraisals and title searches, verifying employment, checking for missing documents. |

| Underwriting | Assess the risk of the loan and make the final approval decision. | Analyzing credit history, debt-to-income ratios, and the property's value; issuing approval conditions. |

| Closing | Finalize the loan, sign all legal documents, and transfer funds. | Preparing the Closing Disclosure (CD), coordinating with the title company, funding the loan. |

Ultimately, a smooth process is a win for everyone. When borrowers are kept in the loop and understand the mortgage loan processing steps, they are far more likely to provide what you need quickly, preventing frustrating and costly delays down the line.

For lenders and brokers, a refined workflow does more than just close loans faster. It builds a reputation for reliability and professionalism, turning a one-time transaction into a long-term client relationship.

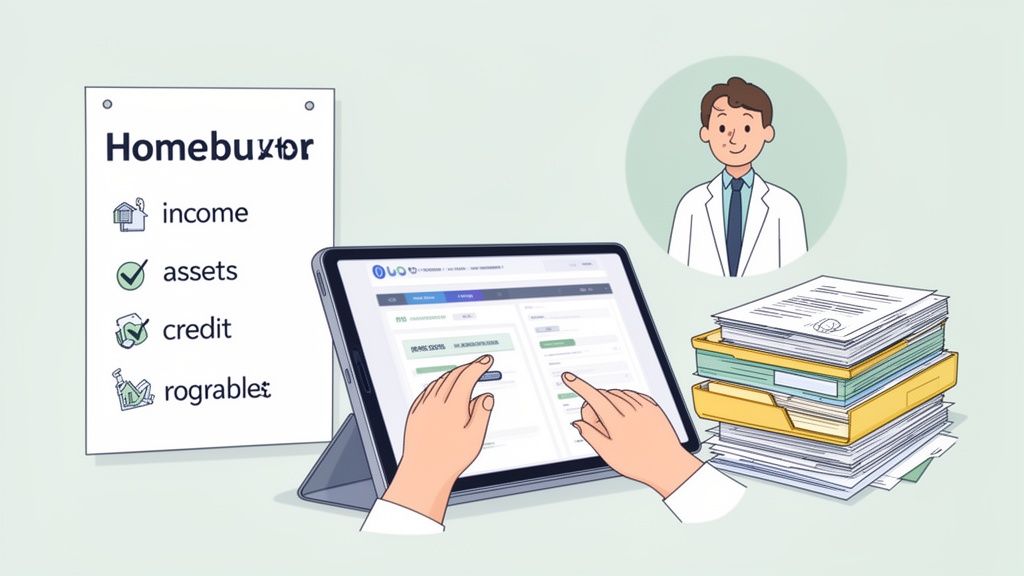

The Application and Pre-Approval Stage

This is where it all begins. Think of the application and pre-approval stage as the foundation for the entire mortgage journey. Everything that follows—processing, underwriting, closing—depends on how well this first step is handled. Getting it right from the start prevents those frustrating delays that can bog down the whole process for both your team and the borrower.

The main goal here is simple: gather all the essential information from the borrower. We're talking about income, assets, employment history, and their credit situation. A complete, accurate application is the golden ticket for a smooth handoff to your processors and underwriters.

Gathering the Right Information from Day One

Let's be honest, the initial document collection can be a real headache. Borrowers, especially first-timers, often get buried in paperwork requests. This is your chance to stand out with a clear, guided approach.

Imagine Sarah, a first-time homebuyer. Instead of hitting her with a generic, mile-long email of document requests, you give her access to a clean, branded digital portal. This isn't just a place to dump files; it actively walks her through what’s needed.

- Pay Stubs: The portal clearly states she needs her last 30 days of pay stubs and lets her snap a picture and upload them from her phone.

- Bank Statements: It requests the last two months of statements and is smart enough to flag any large, unsourced deposits—the kind of thing that will definitely come up in underwriting.

- Tax Returns: The system asks for the past two years of federal tax returns, making sure all schedules and W-2s are included from the get-go.

This kind of organized collection doesn't just make Sarah’s life easier. It gives the loan officer a perfectly structured file, which drastically cuts down on the endless back-and-forth emails. If you need a complete rundown, check out our comprehensive mortgage document checklist.

The Power of Automation in the Application Stage

Modern lending tech has completely changed this game. Lenders who use AI-powered document recognition and automated workflows are no longer spending hours on an application—they're spending minutes. This eliminates redundant requests and gets the file moving.

The numbers don't lie. Recent data shows that platforms integrating these tools have slashed operational cycle times by three full days. They’ve also boosted operational leverage by 23% and increased the gross profit per loan by an average of $1,056.

A strong pre-approval isn't just a number—it’s a powerful tool that gives the borrower confidence and a competitive edge in the housing market. It signals to sellers that they are a serious, qualified buyer.

Once all the initial documents are in and reviewed, the loan officer can issue that all-important pre-approval letter. This letter provides a solid estimate of the loan amount the borrower can expect to qualify for. For the processor and underwriter waiting downstream, a file built on this solid foundation means fewer surprises and a much clearer path to final approval.

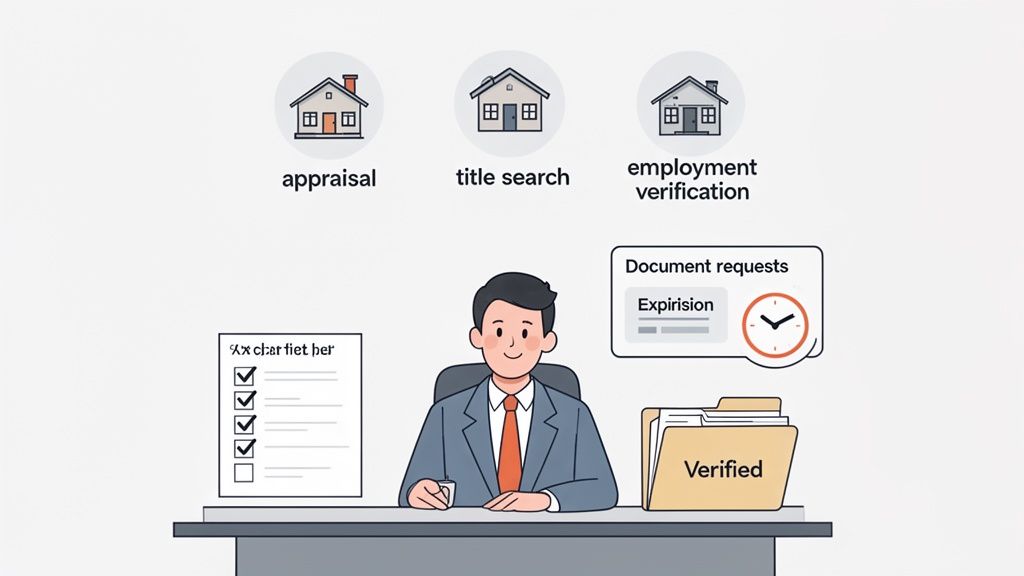

Diving into Loan Processing and Verification

Once the application is bundled up, the file lands on the loan processor's desk. This is where the real detective work begins. Think of the processor as the person who puts the entire puzzle together, making sure every piece of information the borrower provided is checked, double-checked, and verified. Their job is to build a rock-solid loan file that leaves no questions for the underwriter.

This isn't just about paperwork. The processor is also the main point of contact for all the third-party services needed to move the loan forward. They're the ones ordering the property appraisal, kicking off the title search, and sending out those all-important verification of employment (VOE) requests.

Every report that comes back has to line up perfectly with the application. If something's off—like an appraisal that comes in low, a surprise lien on the title, or an employer saying the borrower makes less than they claimed—it can throw a serious wrench in the works.

The Processor’s Playbook: Document Review

A huge part of the processor's role is digging into the borrower’s financial documents. They are the first line of defense, trained to spot potential issues long before an underwriter ever sees the file.

Here's a look at what they're combing through:

- Pay Stubs and W-2s: They’re checking that the year-to-date income makes sense and matches the salary on the application. Any big, one-off commissions or bonuses will get a closer look and likely require an explanation.

- Bank Statements: Processors need to see enough cash for the down payment and closing costs. They're also on high alert for any large deposits that aren't from payroll—every single one has to be explained to prove it’s not a secret loan from a friend or family member.

- Tax Returns: These give the big picture of a borrower's financial health over the last couple of years. For self-employed applicants, this is especially critical for showing stable, reliable income.

A great processor thinks like an underwriter. They don't just verify a document; they anticipate the questions that will come up. By getting a letter of explanation for a recent credit inquiry or sourcing that large deposit from the get-go, they keep the file from getting bogged down in underwriting.

A Day in the Life of a Loan Processor

Let’s put this into practice. Imagine a processor, Alex, gets a new file for a freelance graphic designer. Time is of the essence. Alex immediately kicks off the process, sending a secure request to the borrower for two years of business tax returns and a current profit-and-loss statement.

At the same time, Alex orders the appraisal and sets a calendar reminder to check on its status in seven days. He also notes that the borrower's bank statements are set to expire in 20 days, creating a task to request fresh ones before they do. For a closer look at these modern workflows, you can learn more about how to collect and validate documents.

This systematic approach prevents things from slipping through the cracks. When the appraisal comes back, Alex has already worked with the borrower to document a large payment from a client. The result? A clean, organized file that glides right into underwriting, proving just how crucial a sharp processor is to a smooth closing.

Crunch Time: Navigating the Underwriting Process

After the processor has meticulously assembled the loan puzzle, the complete file lands on the underwriter's desk. This is where the rubber meets the road. The underwriter is the final gatekeeper, the one who gives the ultimate thumbs-up or thumbs-down.

Think of the underwriter as the lender's risk detective. Their job is to protect the lender from bad loans by making absolutely sure of two things: the borrower can repay the loan, and the property is worth the investment. To figure this out, they put the entire file under a microscope, focusing on what we in the industry call the "three C's."

The Three Pillars of Underwriting

An underwriter’s entire review boils down to these three core principles. If you can get ahead of their questions in these areas, you'll sail through.

-

Credit: This is all about the borrower’s track record with debt. The underwriter will pull a fresh credit report and comb through it. They’re looking for a solid history of on-time payments, smart use of credit (low balances), and no major red flags like recent bankruptcies or foreclosures. They'll even dig into recent credit inquiries to make sure the borrower hasn't secretly opened a new credit card to buy furniture for the new house.

-

Capacity: This C answers one simple question: "Can they actually afford this?" It’s not just about having a job; it’s about the numbers. The underwriter calculates the borrower's debt-to-income (DTI) ratio, stacking up their total monthly debt against their gross monthly income. They’ll pore over pay stubs, W-2s, and tax returns to confirm the income is stable and sufficient to cover the new mortgage on top of everything else.

-

Collateral: This is the property itself—the house, the condo, the physical asset. The underwriter dives deep into the appraisal report. Does the home's value genuinely support the loan amount? Are there any safety issues or required repairs noted by the appraiser? They also check that the property type fits the specific loan program's rules.

From Conditional Approval to Cleared to Close

It's pretty rare for a loan to fly through underwriting with zero questions. What's much more common is a conditional approval. This is good news! It means the underwriter is ready to approve the loan, if the borrower can just provide a few more pieces of information.

A conditional approval isn't a rejection; it's a to-do list. The secret is to tackle the underwriter's requests—called "conditions"—quickly and precisely.

So, what kind of conditions pop up? It's usually things like:

- A letter explaining a large, non-payroll deposit in a bank account.

- The most recent pay stubs if the first set is now more than 30 days old.

- Proof that an old collection account has finally been paid off.

Here’s a real-world scenario: An underwriter spots a random $5,000 deposit in the borrower's bank statement. They’ll immediately issue a condition asking for the source. To satisfy this, the borrower provides a signed gift letter from their parents, confirming the money was a gift for the down payment and not a secret loan that has to be paid back.

Once every last condition has been met, documented, and signed off on, the underwriter issues the magic words: "cleared to close." This is the green light everyone has been working for. It means the lender is fully satisfied with the risk and is ready to fund the loan, pushing the file into the final closing stage. A file that was well-prepared from the start makes this final step a smooth and satisfying finish.

Closing and Funding the Loan

You've made it through underwriting, and now you're at the finish line. The final phase in the mortgage process is the closing, and it’s the moment everyone has been working toward. This is where the property officially changes hands, and it’s a step that demands precision and rock-solid coordination to get right.

The star of the show at this stage is the Closing Disclosure (CD). This five-page document lays out the entire transaction in black and white—loan terms, estimated monthly payments, and a complete list of closing costs.

Under federal law, the borrower absolutely must receive and sign off on the CD at least three business days before closing. Think of it as a mandatory "cooling-off" period. It's not optional, and it gives the borrower a crucial window to review everything and clear up any last-minute questions.

What Happens at the Closing Table

With the three-day review period over, it’s time for the closing meeting. This is usually handled by a title company or an attorney, and it’s where the buyer and seller sign the mountain of final documents.

The title company is the neutral party here. Their job is to make sure all the money is collected and paid out correctly. They also confirm the property title is clean—no unexpected liens or claims—before transferring it.

Once all the signatures are on the dotted line, the loan is ready to fund. The lender wires the money to the title company, which then pays the seller and others, like the real estate agents. The county records the new deed, the keys are handed over, and the deal is officially done.

Bringing the Final Step into the Modern Era

Closing used to be a strictly in-person affair, but technology has really changed the game. E-signatures and Remote Online Notarization (RON) are making this last hurdle much more convenient.

Digital platforms have made the closing phase remarkably faster. We've seen timelines nearly cut in half in recent years, and lenders consistently report that borrower portals make for a much smoother handoff. This isn't just about speed; this tech can genuinely cut origination costs and make the entire journey better for the borrower.

Picture a real estate agency trying to coordinate five closings in a single week. Instead of physically chasing down paperwork for each one, they use a central platform. All the final documents are stored securely in one place, which keeps them compliant and gives every client a clean, professional experience.

Having a good system in place for this final stage is non-negotiable. If you're looking to button up your own process, our guide on creating a client document collection portal offers some great insights. It's an approach that not only speeds things up but also creates a clear, auditable trail for every single transaction.

Frequently Asked Questions About Mortgage Processing

Even with the smoothest workflow, questions are going to pop up. The mortgage process has a lot of moving parts, so it's only natural for both borrowers and mortgage pros to need a little extra clarity. Let's tackle some of the most common questions that come up on the road from application to closing day.

How Long Does the Entire Mortgage Loan Process Typically Take?

There's no single magic number, but most mortgages close within 30 to 60 days. What really dictates the speed is a mix of things: the type of loan you're getting, your lender's efficiency, and how quickly you can get your documents in order.

A clean, complete application is your best bet for a fast track. On the other hand, things that can really drag out the timeline include missing paperwork, a property appraisal coming in with issues, or just waiting on third-party companies to send back verifications.

It's worth noting that modern digital workflows are making a real dent in that average. Lenders using up-to-date platforms can often shave significant time off the process simply by cutting down on manual tasks and sidestepping old-school bottlenecks.

What Are the Most Common Reasons for Underwriting Delays?

Underwriting is the stage where a tiny oversight can turn into a major headache. Delays here almost always come from information that doesn’t quite line up or something that makes the underwriter—the person paid to worry about risk—pause.

Here are a few of the usual suspects I see all the time:

- Surprise Debts: That new car loan or credit card that didn't make it onto the original application.

- Mystery Money: A large cash deposit showing up in a bank account without a clear paper trail explaining its origin.

- Gaps in Employment: Unexplained time between jobs can make it tougher to prove a stable, reliable income.

- Appraisal Problems: The property appraisal comes in lower than the purchase price, creating a value gap.

The best way to sidestep these issues? Be an open book with your loan officer from the very beginning. If you know there’s something unusual in your financial history, get ahead of it and provide the documentation. It’ll save everyone a ton of time.

What Is the Difference Between a Loan Processor and an Underwriter?

They work hand-in-hand, but a loan processor and an underwriter have very different roles. I like to think of them as two key players on the same team, each with a specific job to do.

The loan processor is essentially the file's project manager. Their main goal is to collect and double-check every single piece of required paperwork. They're the ones ordering the appraisal, verifying employment, and packaging everything up into a neat, complete file that's ready for a final decision.

Then, the loan underwriter steps in as the decision-maker. They take that perfectly organized file from the processor and put it under a microscope to evaluate the risk. They are laser-focused on making sure the loan ticks every single box in the lender's guidelines before giving the final "yes" or "no." In short, the processor builds the case, and the underwriter makes the final call.

Ready to transform your document collection from a tedious chore into a seamless, professional experience? Superdocu provides the tools you need to automate requests, securely gather files through a branded portal, and keep your workflow moving. Start your free trial today and see how easy it can be.